Global Non Cloud Personal And Entry Level Storage Pels Market

Market Size in USD Billion

USD

152.32 Billion

USD

955.44 Billion

2025

2033

USD

152.32 Billion

USD

955.44 Billion

2025

2033

| 2026 - 2033 | |

| USD 152.32 Billion | |

| USD 955.44 Billion | |

| % | |

|

What is the Global Non Cloud Personal and Entry Level Storage (PELS) Market Size and Growth Rate?

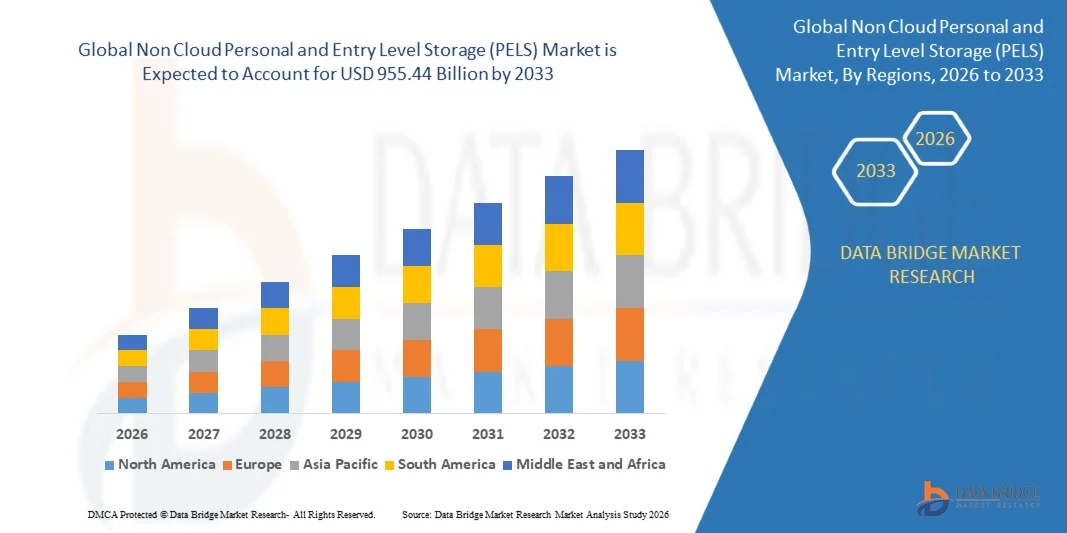

- The global non cloud personal and entry level storage (PELS) market size was valued at USD 152.32 billion in 2025 and is expected to reach USD 955.44 billion by 2033, at a CAGR of25.80% during the forecast period

- The rapidly increasing volume of digital data has been directly influencing the growth of non cloud personal and entry level storage (PELS) market

- Also, the constant increase in the amount of data and growing complexities in handling a large amount of data is also flourishing the growth of the non cloud personal and entry level storage (PELS) market

- In addition, the rising numbers of smartphones, laptops and tablets as well as growing use of online gaming and internet media are also positively impacting the growth of the market

What are the Major Takeaways of Non Cloud Personal and Entry Level Storage (PELS) Market?

- The rising numbers of smartphones, laptops and tablets as well as growing use of online gaming and internet media are also positively impacting the growth of the market

- Furthermore, the rapid expansion of the IT and telecom industry across the world as well as the rapid increase in the data loss cases in several industries and demand for data backup for security are also largely lifting the growth of the non cloud personal and entry level storage (PELS) market

- North America dominated the non cloud personal and entry level storage (PELS) market with a 36.25% revenue share in 2025, driven by strong adoption of advanced computing devices, high-growth semiconductor innovation, and rapid expansion of storage-intensive applications across the U.S. and Canada

- Asia-Pacific is expected to record the fastest CAGR of 9.69% from 2026 to 2033, driven by booming consumer electronics demand, rapid digitalization, and expansion of semiconductor and storage device manufacturing across China, Japan, India, and South Korea

- The Hard Disk Drives (HDDs) segment dominated the market with a 42.6% share in 2025, driven by high storage capacity, affordability, and widespread use for personal backups, multimedia archiving, and small-office data management

Report Scope and Non Cloud Personal and Entry Level Storage (PELS) Market Segmentation

|

Attributes |

Non Cloud Personal and Entry Level Storage (PELS) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Non Cloud Personal and Entry Level Storage (PELS) Market?

“Increasing Shift Toward High-Capacity, Portable, and PC-Integrated Non-Cloud Personal Storage Solutions”

- The non cloud personal and entry level storage (PELS) market is experiencing a growing shift toward compact, high-capacity, and USB-powered storage devices designed for personal data backup, media storage, and lightweight professional use

- Manufacturers are introducing mobile-friendly, SSD-based, and software-integrated storage solutions that offer faster transfer speeds, enhanced data security, and seamless interoperability with PCs, laptops, and tablets

- Rising demand for low-cost, durable, and plug-and-play external storage devices is accelerating adoption across home users, students, freelancers, and small businesses

- For instance, companies such as Seagate, Western Digital, Toshiba, and Samsung have upgraded their personal and entry-level storage portfolios with improved encryption, backup automation, NVMe-based SSDs, and cross-platform usability

- Growing need for personal data management, media archiving, gaming storage expansion, and offline backup is fueling the transition toward faster, lightweight, and portable storage devices

- As digital content consumption rises globally, Non-Cloud PELS products will continue to play a vital role in secure, local, and high-performance data storage

What are the Key Drivers of Non Cloud Personal and Entry Level Storage (PELS) Market?

- Rising demand for affordable, reliable, and easy-to-use external storage devices to support personal data backup, multimedia storage, gaming libraries, and small-office document management

- For instance, in 2025, leading companies such as Seagate, Western Digital, and Solidigm expanded their HDD and SSD portfolios with higher read/write speeds, automated backup features, and enhanced security functionality

- Increasing adoption of high-resolution media (4K/8K videos, gaming content, digital photography) is boosting the need for larger, faster personal storage devices across the U.S., Europe, and Asia-Pacific

- Advancements in SSD architecture, NVMe performance, portable drive durability, and low-power operation have enhanced the efficiency, reliability, and longevity of entry-level storage products

- Growing use of laptops, tablets, smart devices, and home office systems is creating demand for high-capacity, multi-platform USB-C and USB-3.2 storage devices

- Supported by rising digitalization, content creation, and household data generation, the Non-Cloud PELS market is expected to experience strong long-term expansion

Which Factor is Challenging the Growth of the Non Cloud Personal and Entry Level Storage (PELS) Market?

- High pricing associated with large-capacity SSDs and premium portable storage devices limits adoption among cost-sensitive consumers in developing markets

- For instance, during 2024–2025, fluctuations in NAND flash prices, supply chain constraints, and component shortages raised production costs for major storage manufacturers

- Challenges in managing device compatibility, data transfer standards (USB-C, Thunderbolt), and evolving file system formats create technical complexities for end users

- Limited awareness among consumers regarding differences in HDD, SSD, and hybrid storage performance restricts informed purchasing decisions, particularly in emerging economies

- Competition from cloud storage platforms (Google Drive, iCloud, OneDrive) and subscription-based digital storage services reduces reliance on physical personal storage devices

- To overcome these challenges, companies are focusing on cost-optimized SSD models, hybrid storage solutions, security-enhanced firmware, and user-friendly management software to strengthen global market adoption

How is the Non Cloud Personal and Entry Level Storage (PELS) Market Segmented?

The market is segmented on the basis of product, storage system, technology, and end user.

• By Product

On the basis of product, the Non Cloud Personal and Entry Level Storage (PELS) market is segmented into Recordable Discs, Flash Drives, Hard Disk Drives (HDDs), and Solid-State Drives (SSDs). The Hard Disk Drives (HDDs) segment dominated the market with a 42.6% share in 2025, driven by high storage capacity, affordability, and widespread use for personal backups, multimedia archiving, and small-office data management. HDDs remain popular due to low cost per GB and reliability for long-term local storage.

The Solid-State Drives (SSDs) segment is expected to grow at the fastest CAGR from 2026 to 2033, supported by rising demand for high-speed file transfers, portable storage, gaming expansions, and professional media workflows. Increasing adoption of NVMe-based ultra-fast portable SSDs further boosts growth. As personal data volume grows, SSDs will continue gaining market share, especially among high-performance and mobility-focused users.

• By Storage System

On the basis of storage system, the market is segmented into Serial Attached SCSI (SAS), Direct Attached Storage (DAS), Network Attached Storage (NAS), Cloud-Based Storage, and Others. The Direct Attached Storage (DAS) segment dominated the market with a 45.3% share in 2025, as DAS devices—including external HDDs, portable SSDs, and USB flash drives—remain the most commonly used local storage solutions across households, students, freelancers, and SMBs. Their plug-and-play design, low cost, and compatibility with multiple devices drive broad adoption.

The Network Attached Storage (NAS) segment is projected to grow at the fastest CAGR from 2026 to 2033, fueled by rising home offices, personal media servers, surveillance storage, and collaborative data sharing needs. Increasing consumer preference for centralized storage and multi-device synchronization supports NAS expansion. Growing digital content creation and home networking advancements will further accelerate NAS adoption.

• By Technology

On the basis of technology, the Non Cloud Personal and Entry Level Storage (PELS) market is segmented into Magnetic Storage and Solid-State Storage. The Magnetic Storage segment dominated the market with a 58.1% share in 2025, driven primarily by widespread use of HDDs for high-capacity personal data backup, long-term archiving, and offline media storage. Their cost-effectiveness and large capacity options make them the preferred choice for bulk data requirements.

The Solid-State Storage segment is expected to grow at the fastest CAGR from 2026 to 2033, supported by increasing adoption of SSDs, USB flash drives, and NVMe portable storage, which offer superior speed, durability, and power efficiency. As users shift toward faster and lighter devices, solid-state technology is becoming the standard for portable and performance-driven personal storage. Ongoing price reductions in NAND flash are further accelerating the transition from magnetic to solid-state solutions.

• By End User

On the basis of end user, the market is segmented into Banking, Financial Services and Insurance (BFSI), Consumer Goods and Retail, IT & Telecommunications, Healthcare & Life Science, Utilities, Government & Defence, Education & Research, Media & Entertainment, Manufacturing, Business & Consulting, and Others. The Media & Entertainment segment dominated the market with a 21.7% share in 2025, driven by increasing storage needs for high-resolution photos, 4K/8K videos, gaming content, and digital media libraries. Growing demand among content creators, freelancers, and home studios fuels segment leadership.

The IT & Telecommunications segment is projected to grow at the fastest CAGR from 2026 to 2033, propelled by rising data generation, remote work expansion, and the need for high-speed portable storage across IT teams. Increased reliance on local backups, device imaging, and field data storage supports rapid growth. As personal and professional digital workloads intensify, high-capacity PELS solutions remain critical across end-user industries.

Which Region Holds the Largest Share of the Non Cloud Personal and Entry Level Storage (PELS) Market?

- North America dominated the non cloud personal and entry level storage (PELS) market with a 36.25% revenue share in 2025, driven by strong adoption of advanced computing devices, high-growth semiconductor innovation, and rapid expansion of storage-intensive applications across the U.S. and Canada

- Rising deployment of personal data backup devices, external HDDs, SSDs, and USB flash drives in consumer, enterprise, and educational environments fuels regional leadership. Demand is further supported by increasing digital content creation, growing gaming activities, and widespread reliance on high-capacity media storage solutions.

- Strong presence of leading storage manufacturers, continuous product innovation, and high consumer purchasing power reinforce the region’s dominance in non-cloud storage devices

U.S. Non Cloud Personal and Entry Level Storage (PELS) Market Insight

The U.S. remains the largest contributor to North America, driven by strong demand for high-capacity personal storage solutions, increased adoption of SSDs, and rapid expansion of home computing systems. Heavy use of external drives for gaming, multimedia creation, data archiving, and enterprise backup strengthens market growth. A technologically mature consumer base, strong retail distribution networks, and high penetration of laptops, desktops, and consoles support long-term adoption across households, professionals, and small businesses.

Canada Non Cloud Personal and Entry Level Storage (PELS) Market Insight

Canada contributes significantly due to rising remote work adoption, growth in digital education, and increasing use of local storage devices for secure offline backups. Expanding consumer electronics usage, increasing reliance on high-performance SSDs, and growing professional content creation accelerate demand. Government-backed digital transformation, rising tech adoption, and expanding SME activity further support uptake of personal and entry-level storage systems across the country.

Asia-Pacific Non Cloud Personal and Entry Level Storage (PELS) Market

Asia-Pacific is expected to record the fastest CAGR of 9.69% from 2026 to 2033, driven by booming consumer electronics demand, rapid digitalization, and expansion of semiconductor and storage device manufacturing across China, Japan, India, and South Korea. Growing use of laptops, tablets, gaming consoles, surveillance systems, and smart devices fuels large-scale demand for external HDDs, SSDs, and USB flash drives. Rising internet usage, increasing digital content consumption, and strong growth in e-learning and hybrid work environments continue to accelerate adoption of personal offline storage solutions. Cost-effective manufacturing ecosystems and expanding retail availability support long-term regional growth.

China Non Cloud Personal and Entry Level Storage (PELS) Market Insight

China leads Asia-Pacific due to its massive electronics manufacturing ecosystem, strong demand for consumer storage devices, and growing adoption of SSDs across personal computing and gaming. High production capacity, competitive pricing, and large-scale digital content consumption make China a major growth driver. Innovation in NAND flash technology and increasing local PSU and SSD production further strengthen domestic adoption.

Japan Non Cloud Personal and Entry Level Storage (PELS) Market Insight

Japan shows stable growth supported by rising demand for high-reliability storage devices, strong consumer preference for premium SSDs, and increasing deployment of external storage for personal and professional use. High household tech adoption, strong gaming culture, and advanced electronics R&D strengthen long-term market penetration.

India Non Cloud Personal and Entry Level Storage (PELS) Market Insight

India is rapidly emerging as a high-growth market driven by increased laptop penetration, booming smartphone usage, rising gaming activity, and widespread adoption of external storage for education, work, and entertainment. Strong digital transformation initiatives, growing startup ecosystems, and rising disposable incomes accelerate demand for HDDs, SSDs, and USB flash devices.

South Korea Non Cloud Personal and Entry Level Storage (PELS) Market Insight

South Korea contributes significantly due to strong semiconductor leadership, high demand for premium SSDs, and rapid growth in digital lifestyle consumption. Expanding production of memory chips, gaming devices, and smart home systems increases adoption of high-performance external and portable storage solutions.

Which are the Top Companies in Non Cloud Personal and Entry Level Storage (PELS) Market?

The non cloud personal and entry level storage (PELS) industry is primarily led by well-established companies, including:

- NetApp (U.S.)

- Broadcom (U.S.)

- Cisco (U.S.)

- Hewlett Packard Enterprise Development LP (U.S.)

- Hitachi Vantara Corporation (Japan)

- Toshiba Digital Media Network Taiwan Corporation (Taiwan)

- IBM Corporation (U.S.)

- Seagate Technology LLC (U.S.)

- Dell (U.S.)

- Pure Storage, Inc. (U.S.)

- Western Digital Corporation (U.S.)

- Nutanix (U.S.)

- Tintri by DDN, Inc. (U.S.)

- Dropbox (U.S.)

- Scality, Inc. (U.S.)

- FUJITSU (Japan)

- Amazon Web Services, Inc. (U.S.)

- Box (U.S.)

- Microsoft (U.S.)

- OpenDrive (U.S.)

What are the Recent Developments in Global Non Cloud Personal and Entry Level Storage (PELS) Market?

- In May 2024, Dell Technologies unveiled advancements to its Dell PowerStore platform, introducing a multi-cloud storage solution designed to deliver stronger performance, improved data mobility, and enhanced resilience. The upgrade supports rising workload demands and offers flexible storage expansion, ensuring long-term scalability for modern enterprises. This development significantly strengthens Dell’s competitive edge in next-generation storage innovation

- In October 2023, IBM introduced the IBM Storage Scale System 6000, a next-generation cloud storage platform engineered to handle large-scale data processing and high-speed transfers with strong security. Designed to support advanced AI workloads, the system is optimized for storing extensive unstructured and semi-structured data, including text, images, and videos. This launch reinforces IBM’s leadership in AI-driven cloud storage solutions

- In February 2023, NetApp rolled out the NetApp AFF C-Series, a cost-efficient capacity flash storage lineup delivering high-performance all-flash capabilities at lower total cost of ownership. Equipped with ONTAP One, it provides one of the industry's most comprehensive software suites, ensuring operational efficiency, reduced footprint, and improved data management. This introduction marks a major step in NetApp’s expansion of affordable flash storage technologies

- In April 2020, Western Digital announced the WD Black SN850 NVMe SSD, a high-performance storage device built to offer exceptional speed and responsiveness for gamers and content creators. Featuring a PCIe Gen4 interface and available in capacities from 500GB to 2TB, it delivers read speeds up to 7,000MB/s and write speeds up to 5,300MB/s. This product launch positioned Western Digital among the leaders in ultra-fast consumer SSD performance

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.